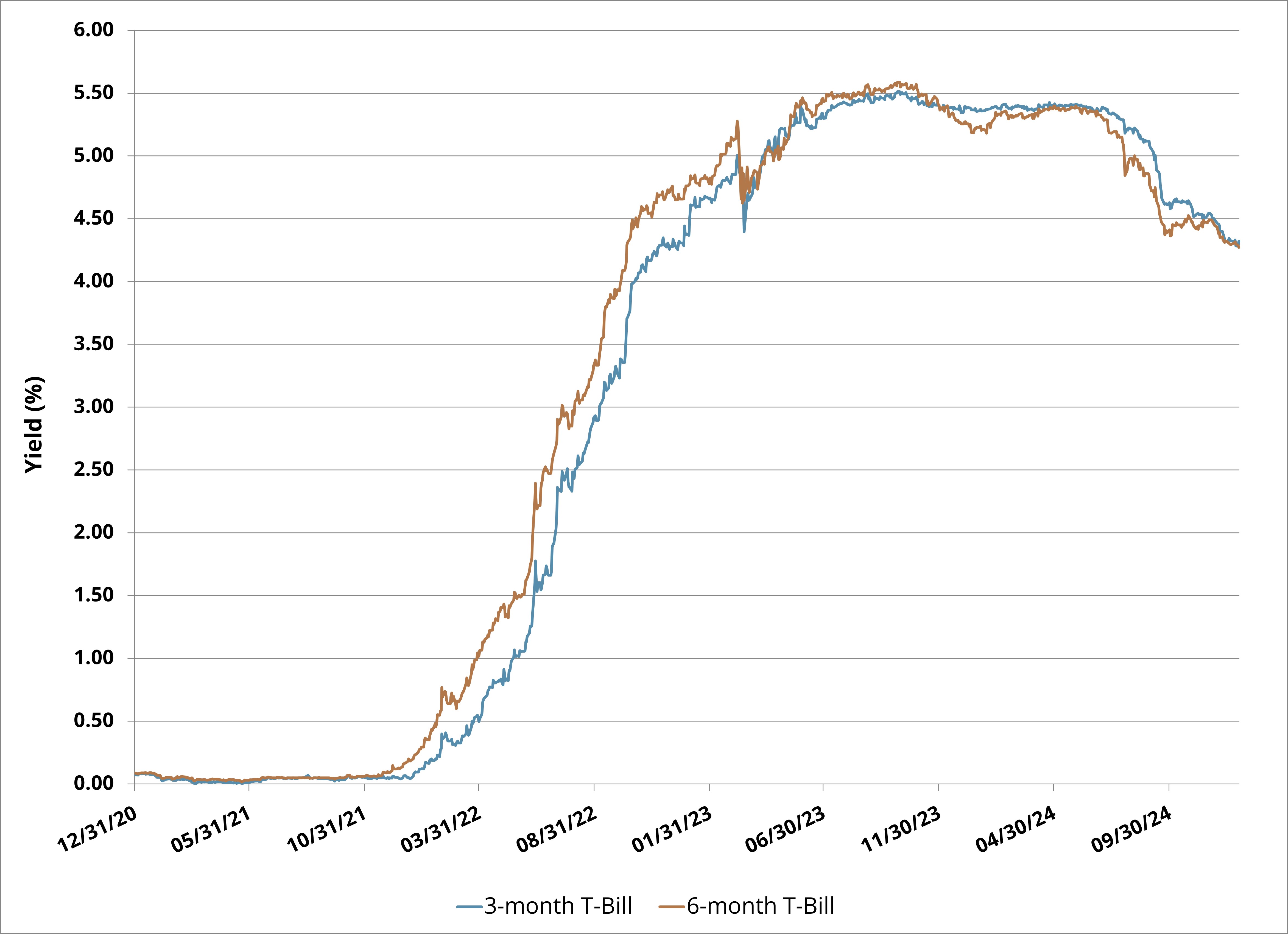

U.S. Treasury Bill yields have been trending lower since last July as interest rate cuts started to be priced into the market. Yields eventually dropped below the psychologically important 5.00% level (see Figure 1) that had many investors hanging out in money market funds for the past couple of years. Then the Federal Reserve Bank (FED) cut the Federal Funds Rate by 100 basis points (bps) over their final three meetings of 2024, beginning the start of an easing cycle that sent Treasury Bill yields even lower. The expected path forward appears to be a gradual pace of interest rate cuts, to bring down the Federal Funds Rate to a more neutral level, and thus Treasury Bill yields should continue to decline. Over $7 Trillion invested in money markets are now searching for a new home and will suffer reinvestment risk the longer an investor waits. In this post, we reintroduce a yield-enhanced Treasury Bill strategy as a cash alternative for those investors still looking for attractive yields without credit risk now that front-end yields are falling.

Figure 1: U.S. Treasury Bill YieldsSource: Bloomberg

Index performance is not representative of fund performance. Past performance is not a guarantee of future results. For the most recent fund performance, (855) 772-8488 or go to www.simplify.us/etfs.

One may not invest directly in an index.

Yield-Enhanced Treasury Bill Fund

The Simplify Treasury Option Income ETF (BUCK) is a yield-enhanced Treasury Bill fund. This ETF looks to maximize Treasury Bill total returns while targeting a duration of one year or less and additionally looks to enhance yield via structural alpha by selling options on Treasuries. The potential yield target is 1.00% to 2.00% higher than the Bloomberg U.S. Treasury Bill: 1-3 Months Index. The fund is actively managed, investing at least 80% of its net assets in U.S. Treasury securities with a duration up to one year, and enhancing income through a risk-managed option selling strategy. The risk-managed options writing strategy is designed to provide additional income as well as add to the ETF’s total returns.

Risk-Managed Options Writing Strategy

Treasury options are consistently in high demand in order for broker dealers – especially those involved with Mortgage-Backed Securities (MBS) – to hedge out interest rate risk. This strong structural demand to buy options naturally increases option premiums, adding to the potential profitability of option selling strategies. By selling out of the money options at key rate levels, BUCK generates additional income while positioning for adding or reducing risk at high reward to risk junctures.

Strike prices in BUCK are typically selected with about a 90% to 95%-win probability that the options expire worthless. Additionally, option durations are short, typically one to two months to expiration. And finally, our risk management procedures will typically close an option early if the position goes in the money, because once an option price goes through the strike price, the move in the option price accelerates rapidly.

Favoring Treasury Volatility over Credit

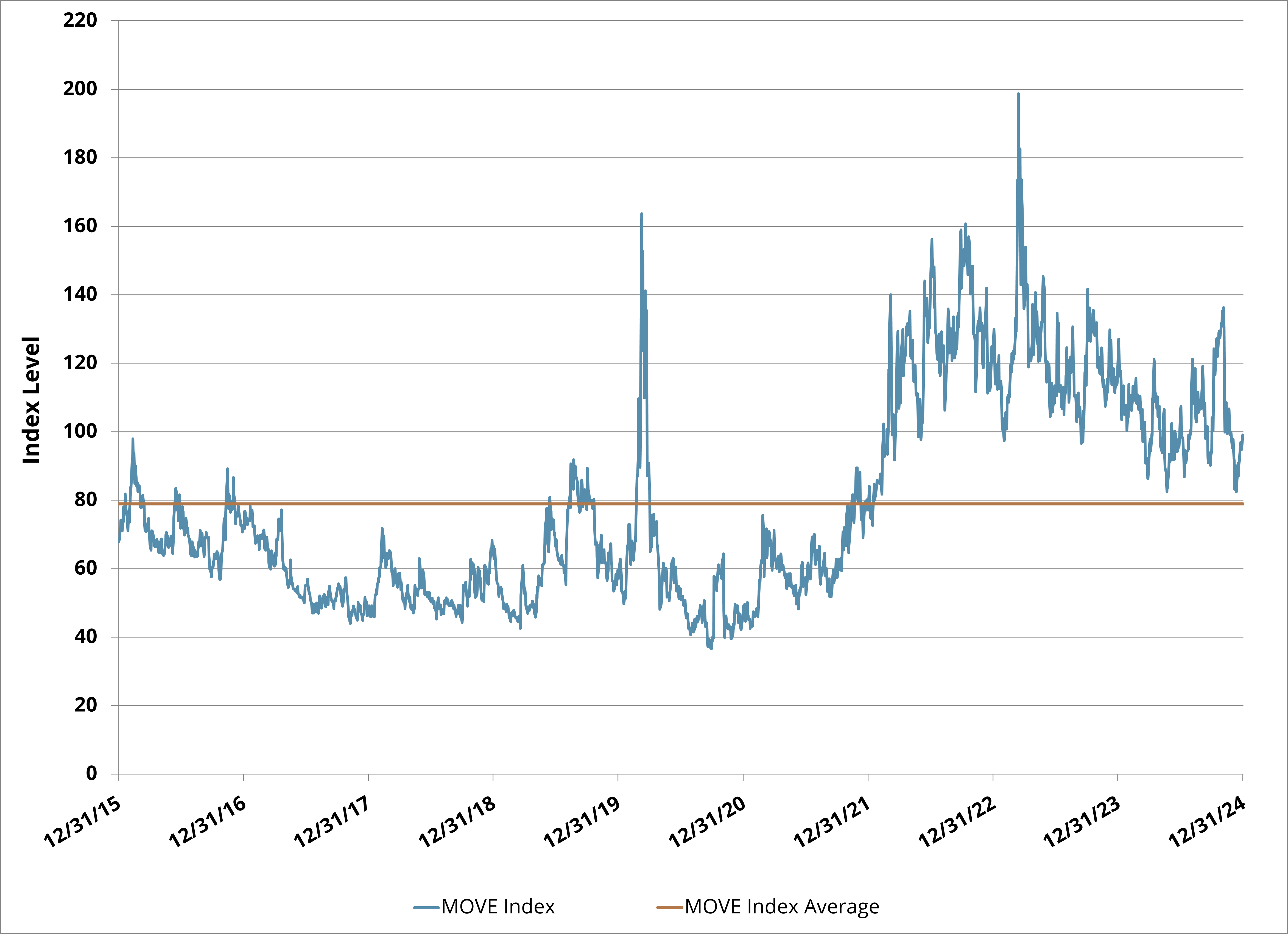

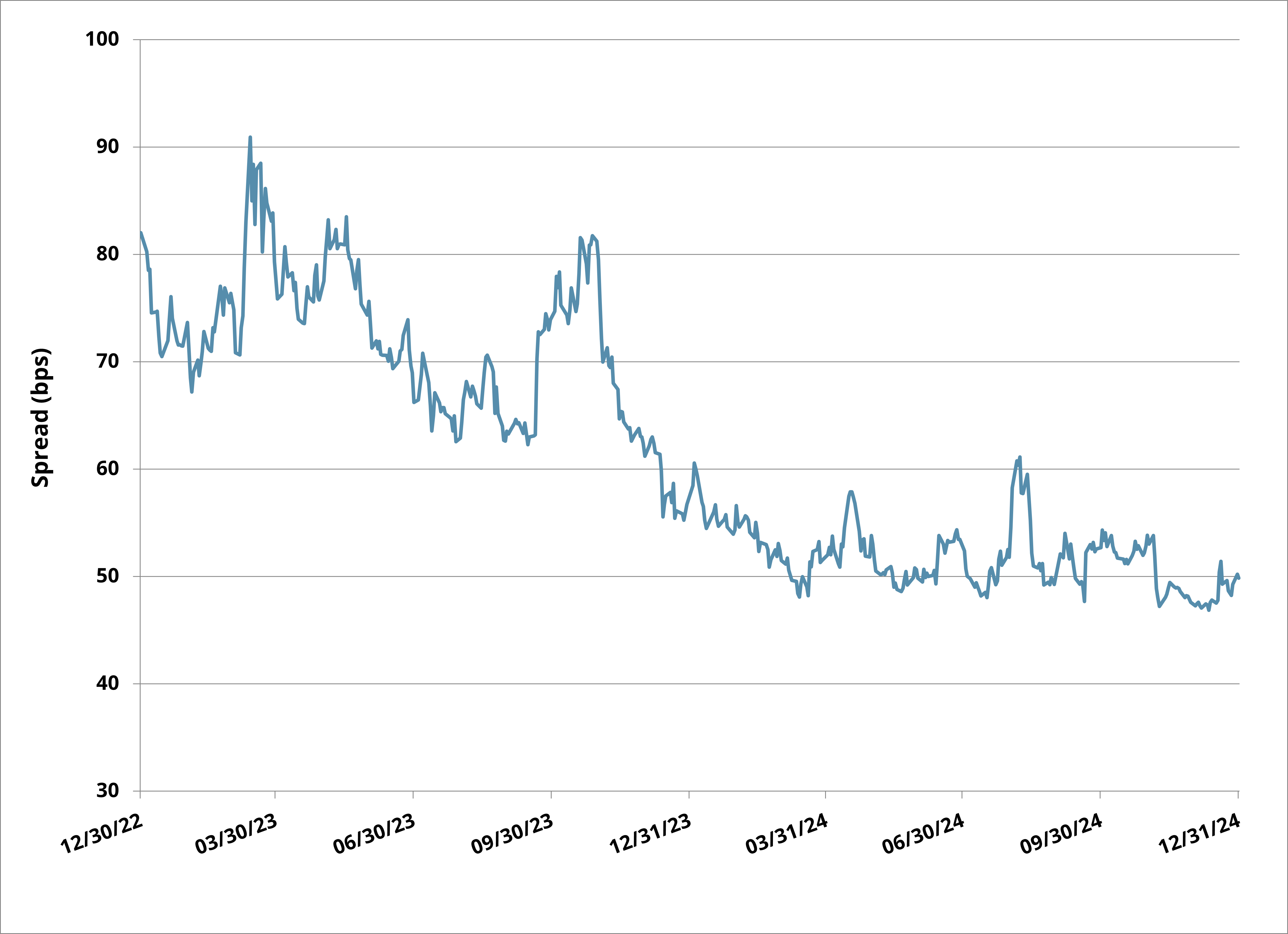

In our view, option-based convexity risk is much more compelling than credit risk right now given that the MOVE Index (created by Simplify’s very own Harley Bassman), remains elevated (see Figure 2) and credit spreads are very tight (see Figure 3).

Figure 2: MOVE Index Remains Elevated, Ripe for Harvesting VolatilitySource: Bloomberg

Index performance is not representative of fund performance. Past performance is not a guarantee of future results. For the most recent fund performance, (855) 772-8488 or go to www.simplify.us/etfs.

One may not invest directly in an index.

Figure 3: 5-Year IG CDX Index Credit Spreads Source: Bloomberg Index performance is not representative of fund performance. Past performance is not a guarantee of future results. For the most recent fund performance, (855) 772-8488 or go to www.simplify.us/etfs.

One may not invest directly in an index.

In Conclusion

The FED has pivoted to a more hawkish stance since their December meeting due to strong economic data, sticky inflation, and uncertainty around fiscal policies of the new administration. This should lead to a more gradual reduction of front-end rates, potentially keeping rates range-bound. However, rates are expected to be volatile within the range, as we have seen over the past quarter, creating opportunities to optimize convexity risk premium via option selling. Most ultrashort duration strategies will enhance yield via credit risk; however, that is not very compelling right now given that credit spreads are very tight. Convexity risk is more compelling, and BUCK seeks to monetize the premium in an optimal way. Investors looking for a cash alternative and willing to accept a small amount of volatility while seeking the highest total returns with an enhanced yield without credit risk should consider an investment in BUCK.

GLOSSARY:

Alpha: An investment strategy's ability to beat the market, or its "edge." Alpha is thus also often referred to as “excess return” or the “abnormal rate of return” in relation to a benchmark, when adjusted for risk.

Basis Points (bps): A common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%.

Bloomberg U.S. Treasury Bill: 1-3 Months Index: Is designed to measure the performance of public obligations of the U.S. Treasury that have a remaining maturity of greater than or equal to 1 month and less than 3 months. The Index includes all publicly issued U.S. Treasury Bills that have a remaining maturity of less than 3 months and at least 1 month and are rated investment-grade. In addition, the securities must be denominated in U.S. dollars and must have a fixed rate. The Index is market capitalization weighted, with securities held in the Federal Reserve System Open Market Account deducted from the total amount outstanding.

Convexity: A measure of how the duration of a bond changes as interest rates change. The greater the convexity of a bond, the greater that change will be for a specific interest rate shift.

Credit Spread: The difference in yield between two debt securities of the same maturity but different credit quality.

Duration: A measure of the sensitivity of the price of a bond or other debt instrument to a change in interest rates.

In the Money: An option that possesses intrinsic value. An option that's in the money is an option that presents a profit opportunity due to the relationship between the strike price and the prevailing market price of the underlying asset.

Mortgage-Backed Securities (MBS): Investment products similar to bonds. Each MBS consists of a bundle of home loans and other real estate debt bought from the banks that issued them. Investors in mortgage-backed securities receive periodic payments similar to bond coupon payments.

MOVE (Merrill Option Volatility Estimate) Index: A measure of expected short-term volatility in the US Treasury bond market.

Option: An option is a contract that gives the buyer the right to either buy (in the case of a call option) or sell (in the case of a put option) an underlying asset at a pre-determined price ("strike") by a specific date ("expiry"). An "outright" is another name for a single option leg. A "spread" is when options are bought at one strike and an equal amount of options are sold at a different strike, all at the same expiry.

Out of the Money: An option has no intrinsic value, only extrinsic or time value.

Strike Price: Strike price is the pre-determined price at which the buyer and seller of an option agree on a contract or exercise a valid and unexpired option. While exercising a call option, the option holder buys the asset from the seller, while in the case of a put option, the option holder sells the asset to the seller. In case of both call and put options, the strike price remains the same through the life of the contract. The difference between the strike price and the current market price (or the underlying price) is one of the inputs that determine the price or premium, which, in turn, decides whether the option is in-the-money or out-of-the-money. Usually, in-the-money options are more expensive than out-of-the-money options.

Total Return: Is the actual rate of return of an investment or a pool of investments over a given evaluation period. Total return includes interest, capital gains, dividends, and distributions realized over a period. Total return accounts for two categories of return: income including interest paid by fixed-income investments, distributions, or dividends and capital appreciation, representing the change in the market price of an asset.

Volatility: A measure of how much and how quickly prices move over a given span of time.