After fourteen long months on hold, the Federal Reserve Bank (FED) cut interest rates by 50 basis points (bps) (0.50%) at their September meeting, delivering an outsized move out of the gate. In his press conference, FED Chair Jerome Powell tried to soothe the market that this larger cut should not be viewed as an emergency cut by stating: “The U.S. economy is in a good place and our decision today is designed to keep it there”, as well as “an appropriate recalibration of monetary policy will help to keep the labor market strong”.

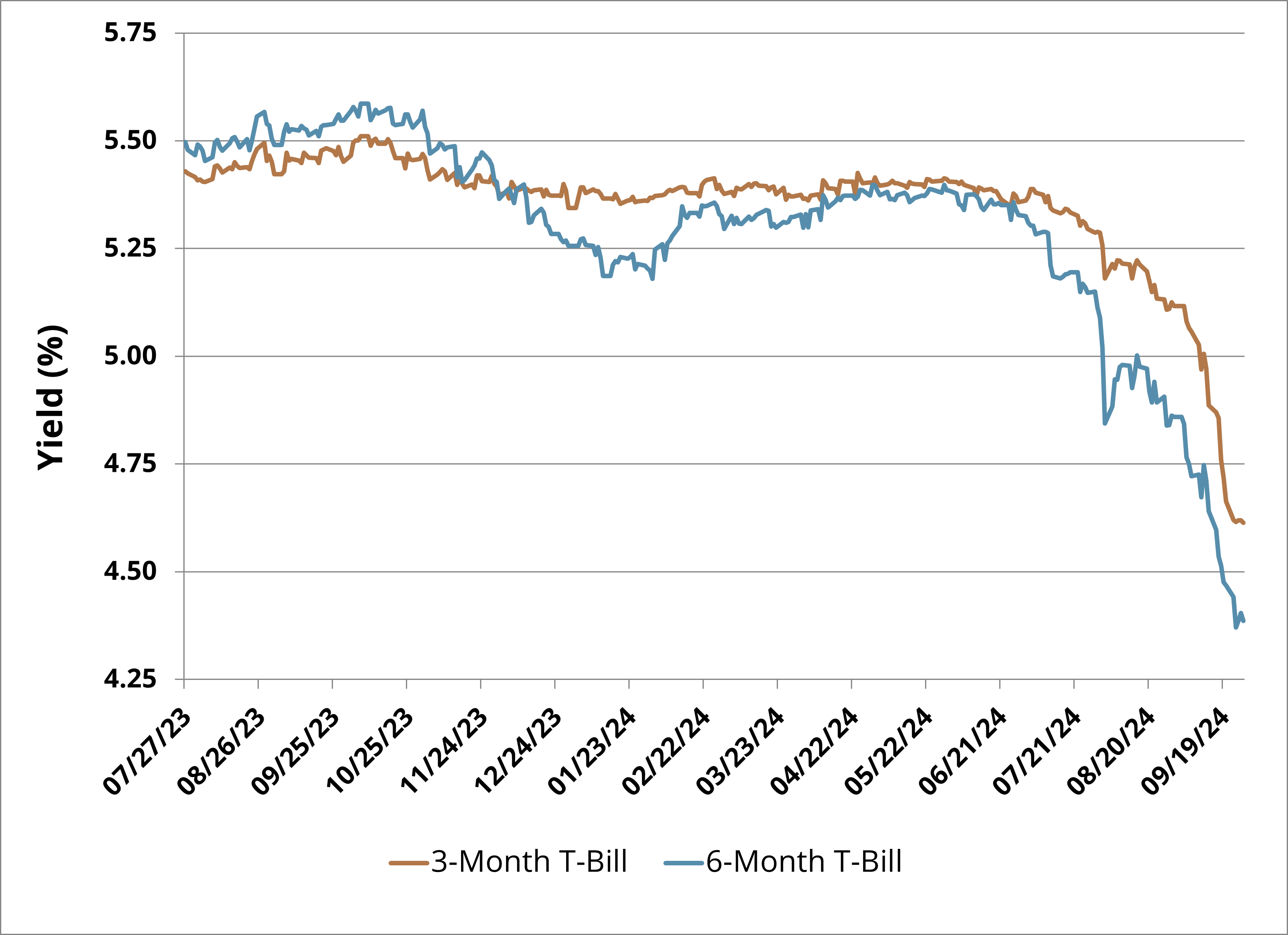

Regardless of your interpretation of the larger cut, the FED has started an easing cycle, and the path forward is a series of interest rate cuts to bring down the Federal Funds Rate to a more neutral level. This means front-end rates will continue to trend lower, especially cash holdings, like U.S. Treasury Bills (see Figure 1), that have benefited the last couple of years from the highest Federal Funds Rate in over 20 years. Thus, the over $6 Trillion invested in money markets will need to find a new home or suffer from reinvestment risk the longer an investor waits.

Figure 1: U.S. Treasury Bill YieldsSource: Bloomberg

Index performance is not representative of fund performance. Past performance is not a guarantee of future results. For the most recent fund performance, (855) 772-8488 or go to https://www.simplify.us/etfs.

One may not invest directly in an index.

Why Are Core Bond Strategies Attractive Now?

With the FED recalibrating its monetary policy, it is time for fixed income investors to recalibrate their allocation to bonds to take advantage of this easing cycle. After two years of being out of favor due to the aggressive hiking campaign to tame inflation by the FED, bonds are now back in vogue with expectations for rates to continue to fall. The bond market has delivered strong returns recently, with the Bloomberg U.S. Treasury Index returning 1.20% in September. This marks five straight months of gains, the longest run since 2010. Now is the time to start extending duration out of the front end and into the intermediate part of the curve, locking in yields as the curve continues to normalize, recently reaching its steepest point since mid-2022. An actively managed core bond strategy can help you manage this recalibration while seeking to maximize total return.

A Better Way to Get Your Aggregate Bond Exposure

The Simplify Aggregate Bond ETF (AGGH) is a yield-enhanced version of the Bloomberg U.S. Aggregate Bond Index. The ETF seeks a higher yield (AGGH 7.00% vs. U.S. Aggregate 4.28%) while also a higher total return with a similar risk profile. Since inception, AGGH has a 1.55% annualized alpha versus the U.S. Aggregate Bond Index as of 10/03/24 (see Figure 2). The fund is actively managed to create a core bond exposure with potential enhanced yield via structural alpha opportunities such as more efficient option writing and curve positioning. The investment process is to buy bonds with the highest risk-adjusted yield, use Treasury futures to set target duration and enhance yield with a risk-managed options selling strategy.

Figure 2: AGGH vs. Bloomberg U.S. Aggregate Bond Index, Cumulative ReturnsSource: Bloomberg

The performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment returns and the principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. For performance data current to the most recent month-end please call (855) 772-8488 or click here. For standardized performance, click here.

Opportunities for Tactical Positioning in AGGH

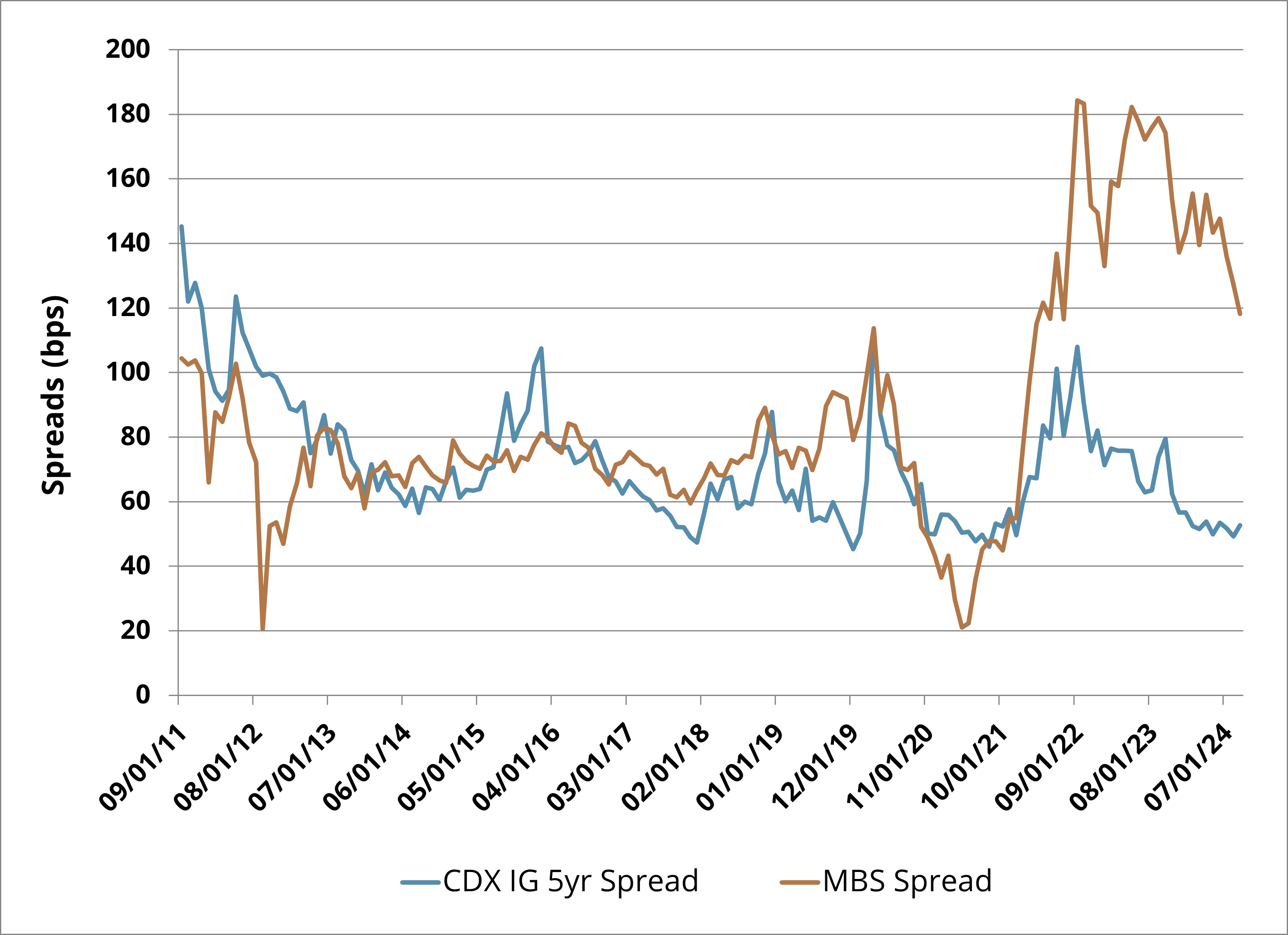

Directional risk in rates is not compelling given forward rates are, in our view, priced fairly. Credit risk is also not very compelling given that credit spreads are very tight. Convexity risk is the most compelling right now and AGGH seeks to monetize the premium in an optimal way. One trade in which AGGH looks to monetize this convexity risk premium is via mortgages by overweighting in the portfolio versus the index while underweighting credit as Mortgage-Backed Securities (MBS) spreads are wider than historical averages (see Figure 3).

Figure 3: MBS Spread vs. IG Credit SpreadSource: Bloomberg

Another way to capitalize on a potentially range-bound fixed income market is through volatility harvesting by selling options on fixed income. This is particularly compelling given that the ICE BofA MOVE Index (created by Simplify’s very own Harley Bassman), the primary measure of U.S. bond market volatility, remains elevated following the 2022 bond bear market and FED rate hiking cycle (see Figure 4). By selling out of the money options at key rate levels, AGGH generates additional income while positioning for adding or reducing risk at high reward to risk junctures. With the FED’s recent cut in interest rates, we expect fixed income short volatility trades to have a tailwind in the coming years.

Figure 4: MOVE Index Remains Elevated, Ripe for Harvesting Volatility

Source: Bloomberg

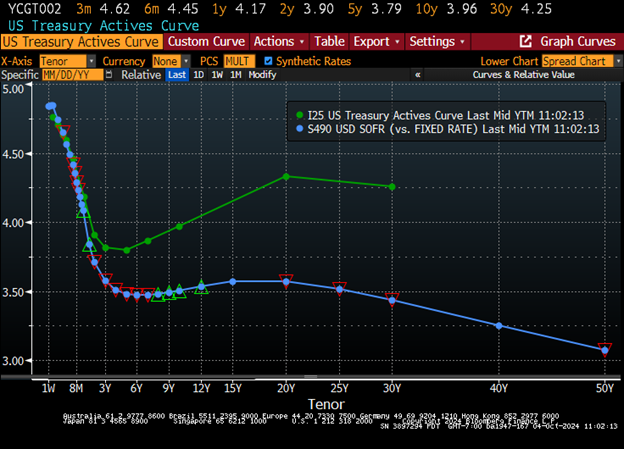

Further opportunities are found in the shape of the Treasury yield curve. One attractive opportunity is buying 20-year Treasury exposure via long bond futures versus paying on 30-year Interest Rate Swaps as the 20-year Treasury is cheap on the curve, especially versus longer-dated swaps (see Figure 5).

Figure 5: U.S. Treasury Active Curve vs. U.S. SOFR Index Swap CurveSource: Bloomberg

In Conclusion

In a FED easing cycle, fixed income should be top of mind and a focal point in a portfolio. Although aggressive market pricing of interest rate cuts has moderated after a strong September jobs report, the FED is still forecasting 150bps (1.50%) of cuts by the end of 2025. This should lead to a more gradual reduction of front-end rates in a range-bound market, however, rates can be volatile within this range around the release of data points thus creating opportunities to optimize convexity risk premium via option selling. Further, credit spreads are near historically tight levels while MBS spreads are providing an attractive alternative to yield with virtually no credit risk. Curve positioning opportunities are also present and available to investors with the right tools and experience to capitalize. Investors looking for broad fixed income exposure in a core bond portfolio with the potential for enhanced yield and seeking higher total return with a similar risk profile to the U.S. Aggregate Bond Index should consider AGGH.

GLOSSARY:

Basis Points: A common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%.

Convexity: A measure of how the duration of a bond changes as interest rates change. The greater the convexity of a bond, the greater that change will be for a specific interest rate shift.

Mortgage-Backed Securities (MBS): Investment products similar to bonds. Each MBS consists of a bundle of home loans and other real estate debt bought from the banks that issued them. Investors in mortgage-backed securities receive periodic payments similar to bond coupon payments.